Texas Redux, America Restrained (With a Discussion of the Limits of Monetary Policy)

February 15, 2012 San Marcos, Texas

Thank you, Lee [Graham] for that kind introduction.

This morning I would like to provide an overview of the Texas economy as we see it from the Federal Reserve Bank of Dallas and then draw some inferences for the nation as a whole.

Texas Redux

In a nutshell, Texas continues on a path it has been on for over two decades, outperforming the nation in economic growth and job expansion. We have fully recovered the jobs lost during the Great Recession and have punched through previous peak employment levels.

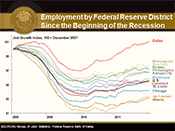

The National Bureau of Economic Research, the arbiter of when recessions begin and end, dates the onset of the Great Recession as December 2007. The economic performance of Texas since December 2007 can be summarized with the chart being projected on the screen. It depicts employment growth in the 12 Federal Reserve districts. In the Eleventh Federal Reserve District—or the Dallas Fed’s district–96 percent of the economic production comes from the 25.7 million people of Texas. As you can see by the red line, we now have more people at work than we had before we felt the effects of the Great Recession. All told, in 2011, Texas created 212,000 jobs.[1]

Only two other states can claim they surpassed previous peak employment levels: Alaska and North Dakota. I do not wish to denigrate the good people of Alaska and North Dakota, but note that their combined population roughly equals that of Travis County.

Readers of this speech abroad—say, in Washington—might think our growth last year came only from the burgeoning oil and gas patch. They would be right to describe it as burgeoning: 30,000 jobs were added in the oil and gas and related support sector last year. And it is correct that with 25 percent of U.S. refinery capacity and 60 percent of the nation’s petrochemical production located in Texas, we benefit from both upstream and downstream energy production. But other sectors outperformed oil and gas in the number of jobs created in Texas in 2011: 58,000 jobs were added in the professional and business services areas, nearly 46,000 in education and health services, and over 41,000 in leisure and hospitality. Manufacturing—which accounts for approximately 8 percent of total Texas employment—added over 27,000 jobs. All told, the private sector in Texas expanded by 266,400 jobs in 2011, while the public sector contracted by 54,800 jobs, due primarily to layoffs of schoolteachers. In sum, Texas payrolls grew 2 percent, significantly above the national rate of 1.3 percent.

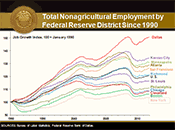

This performance is not unique to last year. As you can see from this second graph of nonagricultural employment growth by Federal Reserve district going back to January 1990, the Eleventh District has outperformed the nation on the job front for over two decades. Note the slope of the top line, which depicts job growth in the Eleventh District compared with all the rest and, importantly, relative to the employment growth rate for the U.S. as a whole–denoted by the black line, the seventh one down.

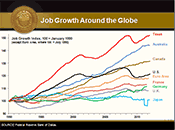

As was pointed out in high relief when a certain Texas governor was briefly in the hunt for his party’s nomination for the presidency, we do have some serious deficiencies in the Lone Star State: We have a very large number of people earning minimum wage; we have an unemployment rate that, while trending downward, is still too high—largely stemming from the fact that our population of workers, including those who are migrating from other states, is growing faster than our ability to create jobs—and many other drawbacks. But I’ll bet you that those who harp on our deficiencies and are given to habitual Texas-bashing would give their right—or should I say, left—arms to have Texas’ record of robust long-term job creation, instead of the anemic employment growth of other mega-states, such as California and New York. Or even compared to other countries! This is a fun chart that will titillate the real Texas chauvinists in the room. It shows that over the past two decades the rate of employment growth in Texas has exceeded that of the euro zone and its two anchors Germany and France, as well as the growth rate of two natural-resource-intensive countries with populations comparable to Texas, Canada and Australia.

Looking Forward

Looking forward, there is good reason to expect continued robust job growth in Texas. The budgetary constraints originally assumed for the state government have proven less severe than originally thought. Due to stronger-than-anticipated tax receipts, it is unlikely employment for schools and other state and local institutions will be cut back as sharply as it was last year. And the Dallas Fed’s Texas Business Outlook Surveys for January indicate that the prospect for job expansion looks promising.[2]

To track the state’s manufacturing industry—which accounts for about 10 percent of the nation’s manufacturing output—the Dallas Fed conducts the Texas Manufacturing Outlook Survey (TMOS). International Strategy & Investment (ISI), a prominent source that tracks, among other things, the various indexes put out by the Federal Reserve, reports that since 2004, the Dallas Fed’s TMOS business activity index has the highest correlation of all Federal Reserve bank surveys with the Institute of Supply Management’s “PMI”—a leading national index of manufacturing activity and sentiment.[3] According to the latest Dallas Fed survey, expectations regarding future business conditions are at an almost 12-month high.

While we have good reason to be proud of our manufacturing prowess, the main driver of the Texas economy is the service sector. It accounts for over 65 percent of private-sector output and employs more than 7 million Texans. To understand trends in the service sector, the Dallas Fed conducts the Texas Service Sector Outlook Survey. According to the most recent survey, the employment index in this survey also signaled an increase in employment levels and in hours worked.

I should add that we are always looking for ways to improve the accuracy of these surveys. As such, if any of you would be interested in participating in our Texas Manufacturing Outlook Survey, please contact me or my staff.

In summary, barring some unforeseeable shock, I would expect Texas to continue leading the nation in job creation.

An Inconvenient Truth

Our record of job growth and the fact that people and companies have been voting with their feet and relocating to Texas from other states illustrate what for some is an inconvenient truth. The citizens of Texas and the Eleventh Federal Reserve District operate under the same monetary policy as do the rest of our fellow Americans. We have the same mortgage rates, pay the same rates of interest on commercial and consumer loans, and our businesses borrow at the same interest rates as our brethren in the rest of the country. Which raises an important question: If monetary policy is the same here as everywhere else in the United States, why does Texas outperform the rest?

The answer is no doubt complicated by the fact that we are blessed with a comparatively great amount of nature’s gifts, a high concentration of military installations and other “unfair” advantages.

For example, if you examine the differences among New York and California and Texas, you will note that these former power states have less-flexible labor rules: We are a right-to-work state; they are not. They have higher population densities: The “Golden State” is 2.3 times as densely populated as Texas; the “Empire State” is four times more densely populated. The cost of housing and the cost of living in both states significantly exceed the cost of living here. Scores measuring the proficiency of middle school students in math are lower in both California and New York than they are in Texas, and in reading, are lower in California and only slightly higher in New York.[4]

Our senior economist and policy advisor Keith Phillips argues that taken together, these are among the important factors affecting where firms choose to locate and hire; these factors also affect where people choose to raise their families and seek jobs.

Fiscal and Regulatory Matters Matter

I would argue that an additional factor favors Texas: We have a Legislature that under both Democratic and Republican governors has over time crafted laws and regulations encouraging business expansion and job creation.

Consider the example of Hardee’s Restaurants. Hardee’s CEO, Andy Puzder, claims it takes six months to two years to secure permits in California to build a new Carl’s Jr. eatery, whereas in Texas it takes six weeks. This is testimony to the fact that the Texas Legislature and local communities are mindful that, as Keith Phillips says, “Government regulations are like prescription drugs: They can improve the quality of life, but in administering them, one must be mindful of their dosage, side effects and interactions.” If the dosage of regulation has the effect of chasing employers away, it is clearly counterproductive to job creation and economic growth.

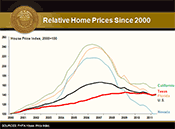

This is not to say that there is no role for prudent regulation. For example, in 1997, Texas lawmakers passed legislation liberalizing home equity lending but limiting homeowner borrowing to no more than 80 percent of their home’s equity. This was no doubt a significant factor in our avoiding the boom and bust of the housing sector, as seen in this chart of the relative performance of home prices since 2000, where Texas is again depicted in the smooth red line.

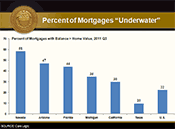

As a result, at present, we have a relatively low percentage of homes that are “underwater,” as shown by this bar chart. Our homeowners are, thus, less burdened with their housing predicament and better positioned as consumers. Indeed, by not allowing our people to use their legally protected homesteads as ATMs, our laws prevented housing from fueling the consumer spending booms and busts seen in the other U.S. states.

I think it is fair to say that the Texas Legislature has conducted the state’s fiscal and regulatory affairs so as to maintain confidence in the future.

Lessons Imparted

One might draw two lessons here.

The first is that Germany’s finance minister, Wolfgang Schäuble, is right when he says, “If you want more private demand, you have to take people’s angst away” by having responsible and disciplined fiscal and regulatory policy. Clearly there is less angst involved in conducting business in Texas.[5]

The second is a broader, macroeconomic truism: That fiscal and regulatory policy either complements monetary policy or retards its effectiveness as a propellant for job creation.

I have noted that under the same monetary policy regime that equally affects all 50 states, Texas has managed to return more quickly to peak employment. I attribute this to several factors but underscore that prudent fiscal and regulatory policy has facilitated our recovery from the Great Recession and for at least two decades, under both Democratic and Republican governorships and legislatures, has helped make Texas a leader in job creation and economic growth.

Monetary Accommodation Is Necessary But Insufficient

Monetary policy provides the fuel for the economic engine that is the United States: As the nation’s monetary authority, the Federal Reserve has made money abundant and cheap for Texans and all Americans. And yet, businesses will not use that abundant and cheap fuel to an optimal degree until they have a clear understanding of how taxes and regulatory and other cost factors will affect their operations going forward. In Texas, they have greater certainty than elsewhere that state and local laws and regulations will encourage investment, business formation and job creation, and this gives us an advantage over many other states. But it is only a marginal advantage, which while important, is insufficient for us to reach our full potential in creating jobs. Federal taxes, spending patterns and regulation weigh heavily on the confidence and capacity of businesses in Texas, as they do elsewhere in the U.S. Ultimately, the key to harnessing the monetary accommodation that has been provided by the Fed lies in the hands of our fiscal and regulatory authorities, the Congress working with the executive branch.

No business operating in Texas or anywhere else in America can properly budget future costs or plan for payroll expansion and capital investment until it knows what its federal taxes will be or how federal spending and regulatory patterns will affect it, its suppliers or its customers. And no one—business operator, worker or consumer—can plan for the long term with confidence until the federal government removes the angst that is associated with runaway deficits and unfunded liabilities that threaten to drown our economy in debt.

In a world driven by rapid technological change and globalization, job-creating capital will flow not only to countries that conduct sound monetary policy but to places with the most welcoming, competitive tax and regulatory systems. This was underscored in a recent Harvard Business School (HBS) survey authored by Jan Rivkin and Michael Porter, two widely admired scholars on national competitiveness and economic development. Their survey of HBS alumni found that the greatest impediments to investing in and creating jobs in the U.S. are the current tax code and regulatory burden and uncertainty, as well as lagging workforce skills. Absent changes on these fronts, the Rivkin/Porter study found that more than 70 percent of respondents expect U.S. competitiveness to decline over the next three years, and along with it, job-creating investment.[6]

No amount of monetary accommodation will change the pathology described by professors Rivkin and Porter. Indeed, excessive monetary accommodation might only add a further dosage of angst, fueling fears of future inflation. Two weeks ago, following the meeting of the Federal Open Market Committee (FOMC), we formally announced that the Federal Reserve has committed to targeting a maximum rate of 2 percent inflation over time. We also announced that we could not be bound by a formal numeric target for employment because “non-monetary” factors determine employment levels, in addition to monetary policy. For me, the message was clear: If we are to heal the plight of the American worker, our fiscal authorities cannot count on the Federal Reserve to do the job only those authorities can do; they must get their act together, set aside their partisan and personal ambitions and act to right their listing fiscal and regulatory ship.

My staff has found a wonderful sketch on YouTube that mimics the action the fiscal authorities have taken thus far. Here it is: http://www.youtube.com/watch?v=Li0no7O9zmE.

That sketch says it all. Whereas before, we used to pass the American dream to our children, we now pass the buck.

Miles To Go Before We Sleep

Now, it is true that businesses that have driven their cost structure to maximum efficiency are beginning again to hire workers with the help of cheap and widely available money made possible by the Fed; the national unemployment rate is beginning to ebb. But too many Americans remain out of work and for too long. We have miles to go before we sleep in the comfort of knowing that the American dream of ever-growing prosperity has been restored.

I would submit that until the fiscal authorities—the Congress and the executive–stop their posturing and their bickering, job creators will sleep only fitfully until they know how decisions about fiscal policy and regulation—if and when they are made—will affect their operations and final demand for their products. And until a credible long-term plan is crafted to bring perpetual deficits and debt accumulation under control, they will be haunted by the nightmare that our elected leaders are simply passing the bill to our children and our children’s children. This is a predicament the Fed is powerless to change.

On that happy note, Mr. Graham, I end. Now, in the best tradition of central bankers, I will do my best to avoid answering any questions you might have.

Notes

The views expressed by the author do not necessarily reflect official positions of the Federal Reserve System.

- According to the National Bureau of Economic Research, the nation went into recession in December 2007 and came out in June 2009. According to the Dallas Fed’s Texas Index of Coincident Indicators, Texas went into the recession in August 2008 and came out in December 2009.

- These surveys can be found on the Dallas Fed website at www.dallasfed.org/research/surveys/index.cfm.

- See ISI’s Daily Economic Report, Jan. 31, 2012.

- See The Nation’s Report Card, http://nationsreportcard.gov/.

- “Q&A: German Finance Minister Takes On Critics,” by Marcus Walker, William Boston and Andreas Kissler, Wall Street Journal, Jan. 29, 2012.

- “Prosperity at Risk: Findings of Harvard Business School’s Survey on U.S. Competitiveness,” by Michael E. Porter and Jan W. Rivkin, Harvard University, January 2012.

About the Author

Richard W. Fisher served as president and CEO of the Federal Reserve Bank of Dallas from April 2005 until his retirement in March 2015.